- Joined

- Jan 12, 2014

- Messages

- 63,441

This is what we’ve needed. A deep pocketed booster that loves the U

I know this dude posts here. Which one are you?

This is what we’ve needed. A deep pocketed booster that loves the U

I know this dude posts here. Which one are you?

Now all started to make sense LOL

That part was very interesting. It's easy to back of the napkin a number*. ((Expected annual volume of collections x average value of collections) x government finder fee) - expenses.

+/- of course.

From a simplistic view, anyone on this board could start a competitor if you know the forms and what database(s) to drag the data from. With that said, Ruiz has concentrated and scaled it.. kudos to him and the organization for recovering all our funds back to the government.

There were also lots of companies some with monoplolies even and other people already picking up people and taking them to other destinations and airports and such.The more I read about the company and what it ostensibly does, the more I am convinced it is some kind of scam. Lots of companies actually are doing this already, there's a whole ecosystem of revenue cycle management companies that work on making sure whoever was supposed to pay does pay. The principals are lawyers that sue insurance companies for reimbursements, but beyond that I don't see a secret sauce here and having no institutional investor participating in a deal that's selling .07% ownership seems like a great way to make yourself a paper billionaire who nevertheless will not be able to become an actual billionaire unless you can find at least $1bn worth of idiots to buy your shares. It reminds me a lot of that sandwich shop in new jersey that's publicly traded and has a $100M float or something ridiculous like that - totally unrealizable for the owner because who is going to pay you $100M for a single sandwich shop in New Jersey? But if you're the owner I guess you get to say that technically, you're worth $100M.

BUT - since at this point all I care about is dollars flowing into UM athletics coffers, I hope this thing somehow pays off big for them and they ride off into the sunset.

Lol. Imagine Krazy with Billions…

There were also lots of companies some with monoplolies even and other people already picking up people and taking them to other destinations and airports and such.

then in came Uber…

#Ya'llBettaBelieveIt

That’s actually a fair stance because I’m sure BOT members have heard it all before.Most of the current BOT have given millions over the years and this guy has given next to nothing. A lot of them think he is full of hot air and won’t come across. They want a big check right now and a pledge of future donations before they listen to him.

Something tells me it’ll become Tootsiesinsight.comLol. Imagine Krazy with Billions…

The entertainment value on here would be… special???

They don’t care about wasting money, which is why they’ll waste a fortune on his softwaredude appears to believe that the government cares about wasting money. pretty crazy assumption imo

I have a very close friend that was involved with this project 5 years ago or so. The consumer isn’t necessarily the gov, but private Medicare/Medicaid administrators… seems like they were in the same place then that they are now.I'd second this call for restraint, at least as it relates to everyone's eyes popping out like the cartoon wolf at the billions Ruiz is supposedly going to be worth - and by extension, the tens or perhaps hundreds of millions UM is potentially going to receive - after the SPAC deal. When his name initially surfaced in the BOT intrigue, I got curious about how a Miami lawyer appeared to have built one of the most valuable tech companies in Florida without anyone ever hearing about it. Turns out I was not the only one curious about this development (from Matt Levine's "Money Stuff"):

SPAC SPAC SPACMan, I don’t know what is going on here, but it’s too weird not to tell you about it. On Monday, a special purpose acquisition company called Lionheart Acquisition Corp. II announced a merger with a company called MSP Recovery LLC, a company “specializing in Medicare Secondary Payer recovery rights and the recovery of improperly paid Medicaid.” Basically someone gets in a car accident, they go to the hospital, Medicare pays their hospital bills, MSP hunts down the auto insurer of the person who hit them, it sues the auto insurer, the auto insurer settles, and MSP pays part of the settlement to its lawyers, gives part to the Medicare provider, and keeps part for itself. That sort of thing. This is more fully explained in the MSP/Lionheart investor presentation.Here is a Bloomberg News article that captures much of the flavor of the deal. Let me select a few numbers from the article to give you a sense:

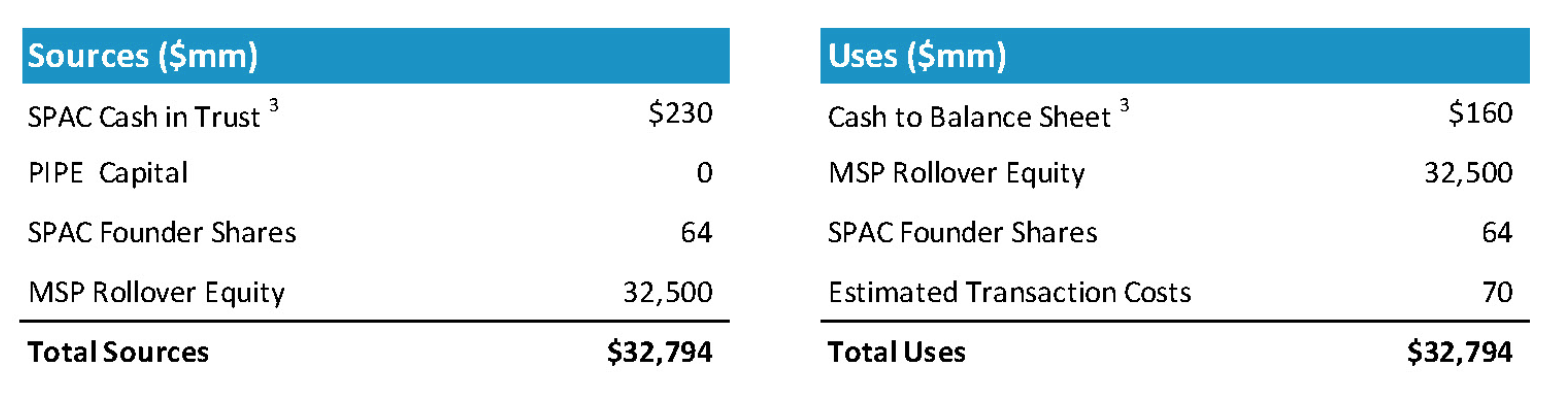

Okay so the key numbers there are “zero revenue” and “at a $32.6 billion valuation, it’s the second-biggest proposed SPAC transaction.” You don’t see a lot of companies with zero revenue and a $32.6 billion valuation. But, you know, fine, some companies have zero revenue and enormous opportunities; maybe it is not that strange for a company with no revenue to raise billions of dollars at an enormous valuation. How much is MSP raising from its deal with Lionheart? Here is the table of sources and uses from the investor presentation: MSP is raising $230 million at a $32.6 billion valuation, and spending $70 million of it on fees. The SPAC’s shareholders are getting 0.7% of the company. Its existing private shareholders are keeping 99%.[1] It gets a $32.6 billion headline valuation by selling $230 million of stock. This is nowhere close to “the second-biggest proposed SPAC transaction,” measured by transaction size. It’s just big measured by headline valuation. MSP is not raising an especially large amount of money, but it’s raising that money by selling a tiny slice of its stock.Actually even that overstates it, because it assumes that Lionheart’s shareholders will all want stock. After a deal like this is announced, the SPAC’s shareholders get to decide whether to roll their SPAC shares into the new company or just get back the $10 in cash that they paid for their shares. Lionheart’s shares closed yesterday at $10.00. That suggests they want their money back.As that Bloomberg article notes, SPAC deals usually come with “traditional co-investors,” institutional investors who buy stock in the company in a PIPE (private investment in public equity). This gives the company more money and greater certainty (because PIPE investors, unlike SPAC investors, do not normally have withdrawal rights), and it helps to validate the SPAC’s valuation: If big institutional investors invest alongside the SPAC on the same terms, SPAC shareholders can have some confidence they’re getting a good deal. This is so traditional that there’s a line for “PIPE Capital” in Lionheart’s sources and uses, even though there isn’t any PIPE capital. I don’t know why that line is there, other than because it was in the bankers’ template and they forgot to take it out. It kind of draws attention to the absence of a PIPE?Also the lack of a PIPE “may be partly due to questions over valuation”[2]:

MSP is raising $230 million at a $32.6 billion valuation, and spending $70 million of it on fees. The SPAC’s shareholders are getting 0.7% of the company. Its existing private shareholders are keeping 99%.[1] It gets a $32.6 billion headline valuation by selling $230 million of stock. This is nowhere close to “the second-biggest proposed SPAC transaction,” measured by transaction size. It’s just big measured by headline valuation. MSP is not raising an especially large amount of money, but it’s raising that money by selling a tiny slice of its stock.Actually even that overstates it, because it assumes that Lionheart’s shareholders will all want stock. After a deal like this is announced, the SPAC’s shareholders get to decide whether to roll their SPAC shares into the new company or just get back the $10 in cash that they paid for their shares. Lionheart’s shares closed yesterday at $10.00. That suggests they want their money back.As that Bloomberg article notes, SPAC deals usually come with “traditional co-investors,” institutional investors who buy stock in the company in a PIPE (private investment in public equity). This gives the company more money and greater certainty (because PIPE investors, unlike SPAC investors, do not normally have withdrawal rights), and it helps to validate the SPAC’s valuation: If big institutional investors invest alongside the SPAC on the same terms, SPAC shareholders can have some confidence they’re getting a good deal. This is so traditional that there’s a line for “PIPE Capital” in Lionheart’s sources and uses, even though there isn’t any PIPE capital. I don’t know why that line is there, other than because it was in the bankers’ template and they forgot to take it out. It kind of draws attention to the absence of a PIPE?Also the lack of a PIPE “may be partly due to questions over valuation”[2]:

What is going on here? I have truly no idea, and I recommend that you read the Bloomberg article, which touches on many weird things I haven’t even mentioned. (“A law firm owned by [MSP Chief Executive Officer John] Ruiz and MSP’s chief legal officer will the exclusive lead counsel for MSP, meaning it stands to receive 20% of all recovered payments, according to a filing.” MSP plans to pay more of its “gross revenue” to its CEO’s law firm than it keeps for itself. That’s weird!)But here’s one way to think of it. If a company can go public at a $32.6 billion valuation, that is helpful for the company and its existing investors. If you go public at a $32.6 billion valuation by selling 10% of your stock for $3.26 billion, that’s great: You have a high valuation and also $3.26 billion. But if you can’t do that, you still get some benefit by going public at a $32.6 billion valuation, even without bringing in any money. If you sell 0.1% of your stock for $32.6 million, then you have a $32.6 billion valuation and essentially no new money. (After paying bankers etc. you are at best breaking even.) But then the next time you try to sell stock, you can say “look, we have a public-market valuation of $32.6 billion.” And then if you sell 1% more of your stock for $326 million, that’s real money. Or if you sell it for $250 million — “we’re giving you a huge discount to our public-market valuation” — that’s real money too.In general you can’t go public at a $32.6 billion valuation by selling 0.1% of your stock for $32.6 million. Even if you could find someone to buy that little stock for that much money, it’s just too weird a deal and your bankers won’t let you. But there are a lot of SPACs out there chasing deals, and if you want to do a weird deal you can probably find a SPAC that will let you.This doesn’t make any real sense as a financial matter, but as a matter of psychological anchoring it does seem helpful for a company with no revenue to be able to say “we went public at a $32.6 billion valuation.” And if that valuation came from selling 0.7% of its shares, and wasn’t validated by any institutional investors in a PIPE, it’s still something. Even if it’s not validated by most of the regular investors in the SPAC, and a lot of them ask for their money back. The Bloomberg article notes:

Is he going to be able to sell that 10% for $3.26 billion? I have no idea. But having headlines saying the company went public for $32.6 billion won’t hurt.

Exec summary: This SPAC deal is extremely unusual, even in the wild wild west world of SPACs. The valuation seems wildly inflated, there are strange potential conflicts of interest between Ruiz and the SPAC founder, the company has essentially no revenue and operates in an extremely uncertain industry (high stakes insurance litigation), there is no large institutional investor to impart their stamp of approval, and most of the wealth created for the founders post-deal appears to be entirely on paper. That's before getting into the regulatory risks endemic to all SPAC deals.

All that said...He sounds like a decently wealthy guy already, he seems highly motivated to make positive changes to the program, and he's cast his lot in with other like minded (and deep pocketed) individuals. I also agree with the sentiment that as long as the money isn't coming from the cartel or Jeffrey Epstein's estate, if it brings us back to national prominence, I don't care whether MSP is the real deal or vaporware. But may be prudent to wait till the deal actually happens before we start spending all that money in our imaginations.

Doesn't hurt to dream I guess, but at the moment I'm pinning my hopes on the more established big money names.

Yeah he only spent 500k on NIL deals for the team this year. Small bones

I'd second this call for restraint, at least as it relates to everyone's eyes popping out like the cartoon wolf at the billions Ruiz is supposedly going to be worth - and by extension, the tens or perhaps hundreds of millions UM is potentially going to receive - after the SPAC deal. When his name initially surfaced in the BOT intrigue, I got curious about how a Miami lawyer appeared to have built one of the most valuable tech companies in Florida without anyone ever hearing about it. Turns out I was not the only one curious about this development (from Matt Levine's "Money Stuff"):

SPAC SPAC SPACMan, I don’t know what is going on here, but it’s too weird not to tell you about it. On Monday, a special purpose acquisition company called Lionheart Acquisition Corp. II announced a merger with a company called MSP Recovery LLC, a company “specializing in Medicare Secondary Payer recovery rights and the recovery of improperly paid Medicaid.” Basically someone gets in a car accident, they go to the hospital, Medicare pays their hospital bills, MSP hunts down the auto insurer of the person who hit them, it sues the auto insurer, the auto insurer settles, and MSP pays part of the settlement to its lawyers, gives part to the Medicare provider, and keeps part for itself. That sort of thing. This is more fully explained in the MSP/Lionheart investor presentation.Here is a Bloomberg News article that captures much of the flavor of the deal. Let me select a few numbers from the article to give you a sense:

Okay so the key numbers there are “zero revenue” and “at a $32.6 billion valuation, it’s the second-biggest proposed SPAC transaction.” You don’t see a lot of companies with zero revenue and a $32.6 billion valuation. But, you know, fine, some companies have zero revenue and enormous opportunities; maybe it is not that strange for a company with no revenue to raise billions of dollars at an enormous valuation. How much is MSP raising from its deal with Lionheart? Here is the table of sources and uses from the investor presentation:MSP is raising $230 million at a $32.6 billion valuation, and spending $70 million of it on fees. The SPAC’s shareholders are getting 0.7% of the company. Its existing private shareholders are keeping 99%.[1] It gets a $32.6 billion headline valuation by selling $230 million of stock. This is nowhere close to “the second-biggest proposed SPAC transaction,” measured by transaction size. It’s just big measured by headline valuation. MSP is not raising an especially large amount of money, but it’s raising that money by selling a tiny slice of its stock.Actually even that overstates it, because it assumes that Lionheart’s shareholders will all want stock. After a deal like this is announced, the SPAC’s shareholders get to decide whether to roll their SPAC shares into the new company or just get back the $10 in cash that they paid for their shares. Lionheart’s shares closed yesterday at $10.00. That suggests they want their money back.As that Bloomberg article notes, SPAC deals usually come with “traditional co-investors,” institutional investors who buy stock in the company in a PIPE (private investment in public equity). This gives the company more money and greater certainty (because PIPE investors, unlike SPAC investors, do not normally have withdrawal rights), and it helps to validate the SPAC’s valuation: If big institutional investors invest alongside the SPAC on the same terms, SPAC shareholders can have some confidence they’re getting a good deal. This is so traditional that there’s a line for “PIPE Capital” in Lionheart’s sources and uses, even though there isn’t any PIPE capital. I don’t know why that line is there, other than because it was in the bankers’ template and they forgot to take it out. It kind of draws attention to the absence of a PIPE?Also the lack of a PIPE “may be partly due to questions over valuation”[2]:

What is going on here? I have truly no idea, and I recommend that you read the Bloomberg article, which touches on many weird things I haven’t even mentioned. (“A law firm owned by [MSP Chief Executive Officer John] Ruiz and MSP’s chief legal officer will the exclusive lead counsel for MSP, meaning it stands to receive 20% of all recovered payments, according to a filing.” MSP plans to pay more of its “gross revenue” to its CEO’s law firm than it keeps for itself. That’s weird!)But here’s one way to think of it. If a company can go public at a $32.6 billion valuation, that is helpful for the company and its existing investors. If you go public at a $32.6 billion valuation by selling 10% of your stock for $3.26 billion, that’s great: You have a high valuation and also $3.26 billion. But if you can’t do that, you still get some benefit by going public at a $32.6 billion valuation, even without bringing in any money. If you sell 0.1% of your stock for $32.6 million, then you have a $32.6 billion valuation and essentially no new money. (After paying bankers etc. you are at best breaking even.) But then the next time you try to sell stock, you can say “look, we have a public-market valuation of $32.6 billion.” And then if you sell 1% more of your stock for $326 million, that’s real money. Or if you sell it for $250 million — “we’re giving you a huge discount to our public-market valuation” — that’s real money too.In general you can’t go public at a $32.6 billion valuation by selling 0.1% of your stock for $32.6 million. Even if you could find someone to buy that little stock for that much money, it’s just too weird a deal and your bankers won’t let you. But there are a lot of SPACs out there chasing deals, and if you want to do a weird deal you can probably find a SPAC that will let you.This doesn’t make any real sense as a financial matter, but as a matter of psychological anchoring it does seem helpful for a company with no revenue to be able to say “we went public at a $32.6 billion valuation.” And if that valuation came from selling 0.7% of its shares, and wasn’t validated by any institutional investors in a PIPE, it’s still something. Even if it’s not validated by most of the regular investors in the SPAC, and a lot of them ask for their money back. The Bloomberg article notes:

Is he going to be able to sell that 10% for $3.26 billion? I have no idea. But having headlines saying the company went public for $32.6 billion won’t hurt.

Exec summary: This SPAC deal is extremely unusual, even in the wild wild west world of SPACs. The valuation seems wildly inflated, there are strange potential conflicts of interest between Ruiz and the SPAC founder, the company has essentially no revenue and operates in an extremely uncertain industry (high stakes insurance litigation), there is no large institutional investor to impart their stamp of approval, and most of the wealth created for the founders post-deal appears to be entirely on paper. That's before getting into the regulatory risks endemic to all SPAC deals.

All that said...He sounds like a decently wealthy guy already, he seems highly motivated to make positive changes to the program, and he's cast his lot in with other like minded (and deep pocketed) individuals. I also agree with the sentiment that as long as the money isn't coming from the cartel or Jeffrey Epstein's estate, if it brings us back to national prominence, I don't care whether MSP is the real deal or vaporware. But may be prudent to wait till the deal actually happens before we start spending all that money in our imaginations.

Doesn't hurt to dream I guess, but at the moment I'm pinning my hopes on the more established big money names.